Table of Contents

How to create a blockchain from scratch is a question many tech innovators ask today. While it may sound complex, with the right approach, it’s entirely achievable.

In today’s fast-evolving digital landscape, blockchain technology revolutionizes how US businesses manage data securely and transparently. From Wall Street financial firms to healthcare providers in California and supply chain giants like Walmart, blockchain is driving operational efficiency, trust, and innovation across industries nationwide. According to recent studies, over 80% of US companies are actively exploring blockchain solutions to enhance data integrity, streamline operations, and comply with evolving regulations.

Blockchain is a decentralised, tamper-proof ledger that records data in blocks, each cryptographically linked and distributed across a peer-to-peer network. This not only enhances security and transparency but also removes the need for traditional intermediaries, enabling faster, more trustworthy digital interactions.

As more U.S.-based startups, enterprises, and public sector entities look to integrate blockchain into their operations, the demand for custom blockchain is growing rapidly. Whether you’re a developer eager to build your own chain from scratch or an entrepreneur looking to launch a blockchain-based product, this blog is your complete guide.

You’ll learn:

A step-by-step process to create a blockchain,

The essential components needed,

Challenges you might face, and

Key technical and strategic considerations.

Let’s dive in and explore exactly how to create a blockchain for your project, from concept to deployment.

How to Build Your Own Blockchain: A Step-by-Step Process

As we discussed, Blockchain applications continue to expand and offer innovative ways to solve complex problems. If you want to create a blockchain, it is essential to know the systematic development process to ensure that the solution meets the specific needs. Here are the key steps to create a Blockchain that stands out in the market.

- Analyze the Blockchain Industry

- Understand the Working process of Blockchian

- Identify and Pick the Best Blockchain Tech Stack

- Find Your Technical Partner

- Create your Blockchain

- Add Unique Features

- Test and Debug Your Blockchain Platform

- Deploy and Maintain the Blockchain

Now let us see it in detail…

STEP 1 – Analyze Your Blockchain Use Case and Industry Landscape

It is the first crucial step in creating a Blockchain application. First of all, you have to analyze the blockchain industry and the use case that you want to target. Blockchain has the potential to disrupt and optimize various industries with unique needs. You can design and develop a Blockchain application by understanding the goals, requirements, and pain points of the industry.

Here are some examples of the industry,

Finance – In this sector, blockchain is used for secure, transparent, and fast transactions. It can support decentralized finance (DeFi), cross-border payments, and secure asset management.

Supply Chain – In the supply chain, blockchain provides end-to-end transparency, tracking the origin and movement of goods. And also it helps to reduce fraud and ensure authenticity.

Healthcare – Blockchain helps secure the sharing of medical records with providers. It also stores patient records and ensures data security, accessibility, and privacy.

Real Estate – In the real estate industry, blockchain helps to streamline property transactions. It provides clear, verifiable ownership records and reduces fraud.

You can create your blockchain application by identifying the challenges and needs of the industry. After you’ve pinpointed the industry, you need to examine the blockchain solutions already on the market. Looking at your competitors helps you see what’s working well and where you might find gaps or chances to improve things.

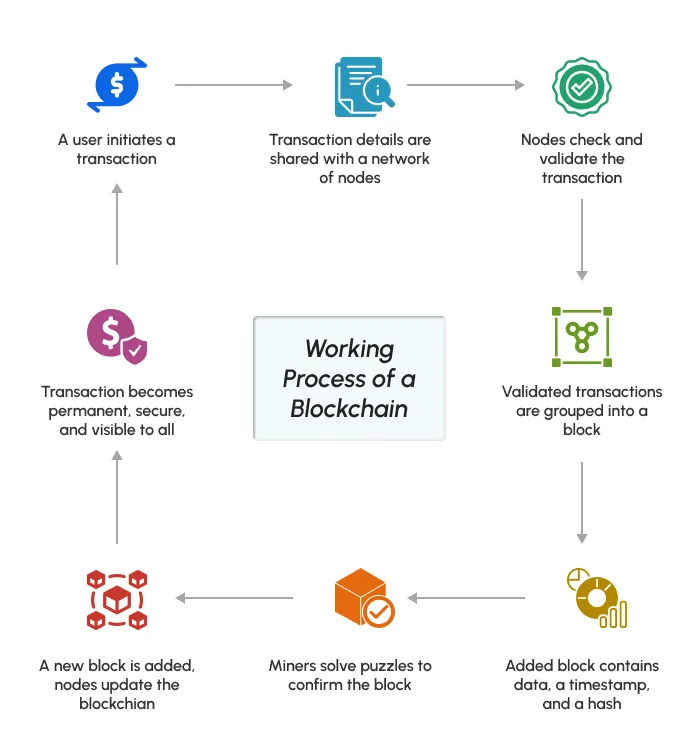

STEP 2 – Understand How Blockchain Technology Works

Understanding the working process of a blockchain is crucial before creating one because it determines how transactions are validated, how secure the network is, how efficiently it operates, and whether it can meet the specific demands of your application.

The consensus mechanism, network design, and participant roles all influence the performance, scalability, and overall success of your blockchain solution.

STEP 3. Choose the Right Tech Stack to Create a Blockchain Application

After you look at the industry and your rivals, you need to pick the right kind of blockchain technology stack, that fits your work process. Also, think about what your project needs, like safety, room to grow shared control, and smooth running.

1. Public Blockchain

Public blockchains are accessible to anyone and operate on a system of shared decision-making. They are designed to function without a central authority, providing unchangeable records and enabling trustless interactions. However, they can encounter issues with scalability and speed when many users try to access them simultaneously.

Examples

Ethereum – Gives strong backing for smart contracts and apps that don’t need a middleman. But it can struggle to keep up when too many people use it.

Solana – Known for quick processing and handling lots of transactions, making it good for apps that need cheap and fast confirmations.

2. Private Blockchain

Private blockchains are permissioned networks controlled by a single organization or group of organizations. They are more expensive than public blockchains but offer more control over workflow and security. Transactions are faster but less transparent.

Example

Hyperledger Fabric – A blockchain that has been approved for enterprise purposes. It allows for the creation of private channels, improving privacy and security while giving organizations control over the process.

3. Consortium Blockchain

Consortium blockchains have also been approved. They are run by a group of organizations rather than a single entity. This type of blockchain balances decentralization and control, making it ideal for industries that require collaboration between multiple trusted parties.

Example

Binance Smart Chain (BSC) – While not fully decentralized, BSC offers efficient transaction processing and is widely used in financial (DeFi) applications. It balances speed, low costs, and some level of integration to improve control and management.

STEP 4 – Find a Trusted Blockchain Development Partner

When choosing a technology partner to build a blockchain solution, look for a team with experience in popular platforms like Ethereum or Hyperledger and strong skills in blockchain development. They should offer customized and scalable solutions while ensuring security and compliance with regulations.

It’s important to find a partner who can handle the entire process, from development to deployment and ongoing support, and who stays up to date with the latest blockchain innovations. Check reviews and testimonials to ensure their reliability, and choose someone who communicates clearly and fits within your budget without sacrificing quality.

STEP 5 – Start Coding: Create the Core Blockchain Architecture

In this section, we will examine the steps your technical partner follows to create your blockchain.

Creating a block

Each block in the blockchain stores related information, including:

- A timestamp indicating when the block was created.

- Change information such as price, sender, and recipient.

- The hash value of the previous block ensures continuity and security.

Blocks are the basic units that make up the blockchain, and all blockchains rely on encryption technology to maintain integrity.

Add the Proof of Work

The proof of work is a mechanism that uses a consensus algorithm. It is used to authenticate the transactions and add the blocks to the blockchain. In PoW, all of a miner would need to do is prove that they have spent considerable time solving incredibly challenging mathematical problems, and a new block can then be added into a chain alongside a number (called a nonce) to achieve proper securities. Proof of Work is a method to protect against fraud. The addition of a block to the blockchain would be a highly costly and daunting proposition and would require computational work and a lot of real power.

Verify the Blockchain

Verification is what ensures the integrity of a blockchain. They have to be checked by the network to see that they are authentic and that it is properly linked to the previous block through its hash value. Only then can we create an immutable tamper-proof record.

Add New changes

Once these changes are acceptable to the user, they get integrated into the blockchain. Trading generally involves the flow of assets (such as cryptocurrencies) between the two parties. It includes details of the sender, recipient, and the amount being sent in every transaction.

Mine New Blocks

Mining refers to the process that validates new blocks through consensus mechanisms like PoW or proof of stake (PoS). As an incentive for keeping the blockchain’s truthfulness, miners are rewarded with coins or tokens for their labor on the network. An important point about mining is that it is used to secure and distribute new blocks for addition onto the blockchain.

STEP 6 – Integrate Unique Features for Your Blockchain Solution

Integrating unique features is the most important step in creating a blockchain. These features make your blockchain unique and stand out from the crowd.

Customizable Consensus Mechanisms – Let users add their own consensus mechanisms to fit different needs.

Interoperability – Make different blockchain networks talk to each other so they can share data easily.

Privacy Features – Add zero-knowledge proofs or private transactions to keep user info and transaction details hidden from public view.

Governance Model – Build in a system where people with a stake can vote on upgrades, rules, or changes to the protocol giving the community more say in how things develop.

Layer 2 Solutions – Add Layer 2 scaling options like side chains or state channels to handle more transactions and cut fees without making the system less secure.

Upgradeable Smart Contracts – Smart contracts can adapt to new needs or fix bugs without disrupting the current system. This flexibility ensures they can meet future requirements.

Built-in Token Economics – A native token system provides incentives, rewards, and penalties. This approach encourages people to take part and keeps the network healthy.

Data Storage Integration – The system links to off-chain storage solutions like IPFS or Filecoin. This setup allows it to store big files or metadata while still connecting to the blockchain for reference.

These additional features can make a blockchain more versatile, efficient, and suitable for a broader range of applications.

STEP 7 – Test, Debug, and Optimize Your Blockchain Platform

Testing is key to ensuring a secure blockchain platform. This helps spot and fix bugs weak spots, and security gaps before the system goes live.

- Unit testing – Checking each part of a block to make sure it works right.

- Integration testing – Making sure the different parts of a blockchain (like transactions, checks, and agreement systems) work well together.

- Security testing – Finding weak spots in the blockchain such as break-in attacks and flaws in coding or data storage.

Proper testing is critical to preventing issues and ensuring the security and integrity of the blockchain.

STEP 8 – Deploy and Maintain Your Blockchain Network

Once it goes live, blockchain systems require ongoing maintenance to remain functional and secure. Maintenance tasks include:

Bug fixing – Fixing issues or errors that occur after deployment.

Performance Improvements—Performance issues may occur over time. Therefore, it is important to optimize the blockchain for speed, stability, and cost efficiency.

Feature Updates—As technology advances, new features and improvements may be required to maintain the blockchain’s relevance. These include new features, improved user interfaces, and adaptation to industry changes.

Security Updates – Security patches and updates are critical to protecting against emerging cyber threats. This ensures that the blockchain remains secure and compliant with regulatory changes.

By following the above-given steps, you can create a blockchain that provides value and meets the needs of your users. Remember that blockchain development is an ongoing process that requires testing, maintenance, and support to remain secure and useful.

Up next, we’ll delve into…

Core Components Required to Build a Blockchain System

To develop a blockchain, several key components must work together to ensure the system operates properly, securely, and efficiently. Here’s a breakdown of the essential components of blockchain.

Block

In a blockchain, a block acts as the primary building block holding a bunch of deals or information. A block splits into two parts: the block header, which is sort of like a label, and the block body where all the transaction deets are stored. Together, these blocks hook up in a chain giving us what we call the blockchain.

Transaction

When we talk transactions, we’re talking about moving info or stuff of value, like that digital money, and crypto, from one person to another. These transactions get packed into blocks and need to pass a crypto check before they can join the blockchain party.

Cryptographic Hashing

Hashing is kind of a brainy way to squish info down to a set size turning it into a string of letters and numbers that’s special just to that piece of info. This cool trick is what keeps the deals secure and stitches blocks together making sure everything stays untouched and legit.

Consensus Mechanism

A consensus mechanism makes sure everyone in the blockchain network is on the same page about which transactions are legit. You’ve got types like Proof of Work (PoW) and Proof of Stake (PoS) that are pretty popular.

Nodes

Nodes are individual computers that make up the blockchain network. These guys are in charge of holding onto and checking the transactions. Full nodes have the whole blockchain on them, but light nodes don’t; they just carry a bit of the blockchain and rely on the full nodes to back them up.

Distributed Ledger

It refers to the blockchain’s database. This thing is kept up by all the nodes together. Each one has its own copy of the ledger, which makes sure everything’s out in the open and secure.

Smart Contracts

Smart contracts automatically execute contract terms when predefined conditions are met, making transactions more efficient and secure. They are widely used to power decentralized applications (DApps) on platforms like Ethereum. As businesses explore smart contract development, these self-executing agreements continue to revolutionize various industries.

Public and Private Keys

Cryptographic keys public and private, guard transactions. Folks use the public key to get funds or info, and the private key makes transactions okay and shows who owns what.

P2P Network (Peer-to-Peer Network)

In a P2P network, folks can link up without a big boss in the middle. It’s a way for them to share stuff and chat.

Token

A token represents ownership, access, or value in a blockchain network. People use tokens in cryptocurrency systems or decentralized apps (DApps) to do transactions or get access.

With these blockchain components in mind, let’s delve into the factors that determine the success of the Blockchain success from the start.

Key Considerations Before You Create a Blockchain

Blockchain technology has emerged as a game-changer in various industries, offering secure, decentralized, and transparent solutions. Building a blockchain from scratch requires careful planning and strategic decision-making. Whether creating a custom blockchain or exploring dApp development, considering key factors can ensure a seamless and efficient implementation.

- Scalability – Scaling the blockchain to accommodate the growing number of users and transactions successfully.

- Compliance – Especially concerning the proper laws, both local and global, to avoid any legal problems.

- Energy Efficiency – Reduce energy consumption by sustainably fine-tuning the consensus mechanisms.

- User Experience – Ensure an enticing as well as user-friendly interface, one that will lead to acceptance.

- Security – By implementing the right cryptographic techniques towards fraud and cyberattack mitigation.

- Cost Efficiency – Eliminating intermediaries lowers transaction fees, making operations more cost-effective. This is a key factor to consider when evaluating the cost to develop blockchain.

- Transparency – As it aids in trust assurance among consumers, the system should be transparent and audit-friendly.

- Customization – Tailor the blockchain to suit the particular needs and requirements of your business or industry.

As you embark on this journey, it’s important to be aware of potential obstacles that could arise. Let’s explore…

Common Challenges in Developing Blockchain (And How to Overcome Them)

- Developing a blockchain is indeed a complicated process, and this complexity has associated challenges. Scalability is a significant challenge in blockchain development, especially in public blockchains. As the user base grows and transactions increase, maintaining performance and speed becomes difficult.

- Every node in a public blockchain must process and store all transactions, leading to slower transaction times and higher costs. To address this, adopting scaling solutions such as sharding or Layer 2 technologies is crucial for improving performance and efficiency.

- Another key challenge is regulatory compliance, as blockchain applications often span multiple jurisdictions. This requires adherence to both international and local laws, including stringent regulations on data privacy (e.g., GDPR) and financial compliance.

- Additionally, security vulnerabilities, such as hacking risks or weak cryptographic implementations, can compromise the blockchain’s integrity. Robust security measures, careful planning, and adherence to legal frameworks are essential to ensure a secure and compliant blockchain system.

Creating a blockchain can be complex, especially for those new to Blockchain technology. If you’re a beginner, partnering with a professional blockchain development company can simplify the process. Pixel Web Solutions, a trusted Blockchain development company is here to help you design and implement a blockchain solution tailored to your business needs.

Transform Your Blockchain Ideas into Success With Us

Pixel Web Solutions Stands out as a prominent firm by offering expertise, innovation, and a customer-centric approach. With a team of skilled developers and a deep understanding of blockchain technology, we deliver tailored solutions that align with your business goals. We ensure that your blockchain solution is robust and future-proof.

Whether you’re looking to enhance energy efficiency, create a user-friendly design, or ensure you meet all necessary regulations, we have the experience and resources to bring your ideas to life. Choose us for reliable support, cutting-edge technology, and a smooth development process that helps you succeed in the exciting world of blockchain.

FAQs on How to Create a Blockchain

Can I Create My Own Blockchain Network From Scratch?

Yes, you can create your own blockchain network from scratch by defining its protocol, setting up nodes, and developing consensus mechanisms tailored to your use case. Ownership depends on how decentralised and permissioned your blockchain is.

How Much Time and Cost Does It Take to Build a Blockchain Network?

The time and cost to build a blockchain network depend on factors like the project’s complexity, development resources, and the type of blockchain you choose to create.

What Are the Different Types of Blockchain I Can Build?

The four main types of blockchain are public, private, consortium, and hybrid—each offering varying levels of decentralisation, access control, and scalability.

How Can I Create and Deploy a Blockchain Application or Network?

To create and deploy a blockchain, you design the architecture, write smart contracts, configure nodes, and deploy the network on a public or private infrastructure using platforms like Ethereum or Hyperledger.

How Do I Start Building a Private Blockchain for My Business?

You can create a private blockchain by first selecting a suitable framework such as Hyperledger Fabric or Quorum, then defining access rules and setting up a permissioned network tailored to your organisation’s internal requirements.